Central banks, politicians and bankers have turned global investment arena into a casino

PREDICTIONS are a waste of time in today’s volatile global markets. Rather than follow usually wrong central bank prognosis, economists’ forecasts, chartists’ configurations or charlatan soothsayers, it is safer to assess the situation on the basis of what is happening here and now.

Current news reports, anecdotes, in-depth investment analyses and healthy scepticism for dated statistics are the necessary tools to gauge risks against potential rewards. After the market depression of late 2008 to 2009, the subsequent steep bull market and this year’s small correction, the following maxim applies: ‘If in doubt, stay out!’

Now, more than ever, institutional and retail investors need to be on their guard against frantic banker and broker advice. The investment bank business is under acute strain. Volatility is driving away customers. Trading volumes and commissions have fallen sharply and investment bank proprietary traders are struggling to cope with unpredictable price gyrations. The result is that investment and private bankers are under severe pressure to encourage clients to either overtrade or buy hedge funds and other products.

The antidote for the investor is to stand back and carefully assess the risks and current values. Even though money is being offered at almost zero interest, it is better to be liquid and await opportunities than to hold a sliding asset. Nifty traders can scalp gains by buying and selling within narrow 5% to 10% trading bands. But they need to be right at least 70% of the time, otherwise all their efforts will be swallowed by commissions and taxation.

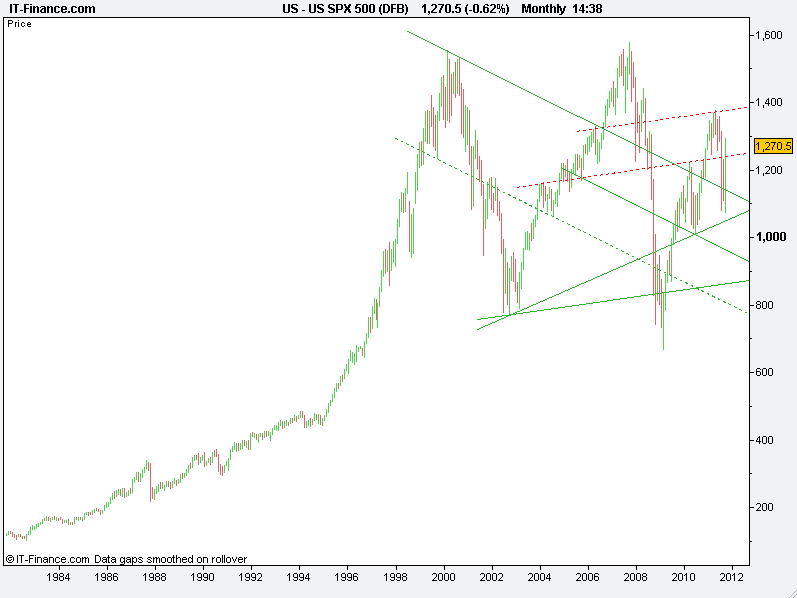

Dirt Cheap in Bear Market, but after 2009-2011 bull market what now?

Why markets have become more risky

Here are some of the main reasons why currency, equity, bond and commodity markets have become increasingly risky and exceedingly difficult to forecast.

Much has been written about the Greek and European crisis in recent weeks and the €1.2 trillion ($1.7 trillion) exposure of the European Central Bank (ECB) and German, French, British and other commercial and investment banks, along with the coming $1 trillion exposure of the European Financial Stability Facility (EFSF), the European bailout fund. In other words the Eurozone will have two big bad banks! Excessive borrowing of both developed and emerging nations are another concern. Geo-political worries about Iran and the rest of the Middle East persist, while Japan is still struggling following the tsunami and Fukushima nuclear power plant disaster and has had to intervene to weaken the overvalued Yen.

The two main economic and financial risks in global markets, however, are the Federal Reserve Board’s monetary policy and China’s imploding bubble.

Fed Chairman Ben Bernanke’s initial liquidity injection helped ease the 2008 credit crunch, but his subsequent quantitative easing (QE) programmes in 2009 and 2010 have created a host of global problems. QE is an untried and reckless monetary experiment from the Fed and Bank of England while the ECB is applying it through the back door.

In essence, these central banks purchase hundreds of billions of bonds from banks and other institutions and investors, and the money flows into the banking system. Interest rates have been kept at almost zero levels for banks borrowing from central banks.

QE Causes Mal Investment, i.e. Misallocation of Capital

The aim has been to bolster economies and reduce unemployment. QE succeeded in boosting US and global shares and corporate bonds from their 2008-2009 bear market lows. This helped raise confidence and enabled companies to raise capital. QE, unfortunately, also has inherent weaknesses.

Since the Fed has been purchasing government bonds, it has been monetising the state’s debt. The flood of money into the banking system has caused US dollar devaluation and consequently a surge in prices of oil and other commodities, and contributed to an increase in global inflation. Prices have fallen from peaks but are still uncomfortably high.

Banks have used the money to speculate in foreign currencies and commodities and encouraged their customers to do the same. QE thus caused ‘mal investment’, or misallocation of capital and a business climate that did not bolster job-creating businesses.

In the meantime, confidence and consumption slid because higher energy prices and inflation have been an effective tax on the consumer. Retired people relying on income have been panicked and are risking their hard-earned savings. Banks charge corporations and individuals much higher rates and since they are encumbered by many dud loans, they have a much stricter lending policy.

The ‘misery index’ of stubbornly high unemployment and inflation has turned sharply upwards. QE has also caused instability in Asia as funds poured into Singapore and other nations, followed by inevitable increases in property prices and inflation.

China’s risks relate to both bubble and fears of corruption

China, a semi-command economy, also embarked on stimulation and monetary ease to counter recession early in 2009.

Now the authorities are trying to curb monetary excess, inflation and wild speculation in property, gold and commodities.

Global investors have also become alarmed by numerous reports of listed China companies’ opaque account keeping. Since growing numbers of China’s directors are allegedly issuing crooked reports, global investors are becoming worried that the authorities are also rigging economic statistics.

Several Western economists and business people are maintaining that China’s business conditions are deteriorating. They do not believe the propaganda of the regime and allege that it is overstating growth and under-reporting inflation.

Anecdotes are doing the rounds of suppressed protests about the high cost of food and goods while corrupt wealthy businessmen and officials are living the high life. Some have contravened exchange control regulations and have funnelled money into real estate, art and various funk holes.

Market gyrations are warning signals that economies are slowing

Wild market fluctuations in recent months are a warning sign that investors are worried about America’s QE failures and events in China and Europe. The tide has begun to turn as investors have become fearful of high-priced financial assets and commodities.

Markets are up one day and down the next as whipsawed investors and traders grapple with unpredictable moves and fear economic downturns and a decline in corporate profits.

These are classic danger signs for long-term investors. Foolhardy, closeted central bankers, China’s authorities and US and European politicians and bankers have turned the global investment arena into a casino